The stock market ended an upbeat week on a positive note. The Dow Jones Industrial Average (+0.8%) paced the advance while the S&P 500 gained 0.5%. The Nasdaq (+0.1%) lagged, but was able to finish at its highest level since late 2000.

Today's advance capped an impressive week during which the benchmark S&P 500 gained 2.3%. Even though stocks rallied sharply, it is worth noting that all five sessions of the week saw below-average volume while bellwether groups like financials and transports struggled to keep pace with the broader market. The financial sector added just 0.2% on Friday, extending its weekly gain to 1.6%. For its part, the Dow Jones Transportation Average (+0.3%) added 0.9% for the week.

Similar to financials, other top-weighted sectors like health care (+0.4%) and technology (+0.2%) lagged while consumer discretionary (+0.6%), energy (+1.5%), industrials (+0.7%), and materials (+0.7%) picked up the slack.

The energy sector drew considerable strength from its largest member, ExxonMobil (XOM 94.11, +2.68), which surged 2.9%. The Dow component regained its 100- and 200-day moving averages in a move that was aided by an ISI Group upgrade to ‘Buy' from ‘Neutral.' On a related note, crude oil ended little changed at $100.29/bbl.

Elsewhere among commodities, precious metals remained on a torrid pace. Gold futures posted their seventh day of gains, climbing more than 5.0% in that timeframe. Meanwhile, silver capped an eight-day run that saw the metal jump nearly 8.0%. This translated into another strong session for gold miners as the Market Vectors Gold Miners ETF (GDX 26.35, +0.48) rose 1.9%.

Mining shares contributed to the outperformance of the materials sector, which also benefitted from gains among steelmakers after Cliffs Natural Resources (CLF 23.16, +1.26) reported better-than-expected results.

Staying on the earnings theme, apparel retailer V.F. Corp (VFC 56.85, -3.04) slumped after announcing disappointing results and issuing a profit warning. The stock tumbled 5.1%, which kept a lid on its peers. The rest of the discretionary sector held up well with help from homebuilders. The iShares Dow Jones US Home Construction ETF (ITB 25.21, +0.28) rose 1.1%.

Interestingly, builder shares outperformed even as Treasury yields inched higher. The benchmark 10-yr yield rose one basis point to 2.74% after ending last week at 2.68%.

As mentioned earlier, trading volume was well below average with only 609 million shares changing hands at the NYSE. Today's final tally represented the lowest total since January 3.

Today's economic data included three reports:

- Export prices, excluding agriculture, ticked up 0.2% in January after increasing 0.3% in the prior reading. Excluding oil, import prices rose 0.3%, which follows last month's downtick of 0.1%.

- Industrial production declined 0.3% in January after increasing 0.3% in December while the Briefing.com consensus expected an increase of 0.3%. Once again, the hard economic data did not mesh with the results in the ISM report and the related regional surveys. Those reports showed solid, albeit slightly unsteady production levels in January. Instead of translating into slightly positive growth, however, actual manufacturing production fell 0.8% in January. That was the largest drop since May 2009. Making matters worse, manufacturing production growth was revised down for each month going back to October. After the revisions, fourth quarter manufacturing production only increased 4.2%, down from an originally reported gain of 6.2%. This comes after the ISM Production Index was recorded above 60 during that entire time, suggesting manufacturers are definitely not doing what they are saying in the surveys. The motor vehicle sector was hit especially hard in January. Assemblies fell by 1.0 million, from 11.64 million in December to 11.62 million in January.

- The preliminary reading for the University of Michigan Consumer Sentiment Index for February was unchanged at 81.2 while the Briefing.com consensus expected the index to fall to 80.2. The Current Conditions Index weakened slightly, falling from 96.8 in January to 94.0. This was offset by an increase in the Expectations Index from 71.2 to 73.0 in February.

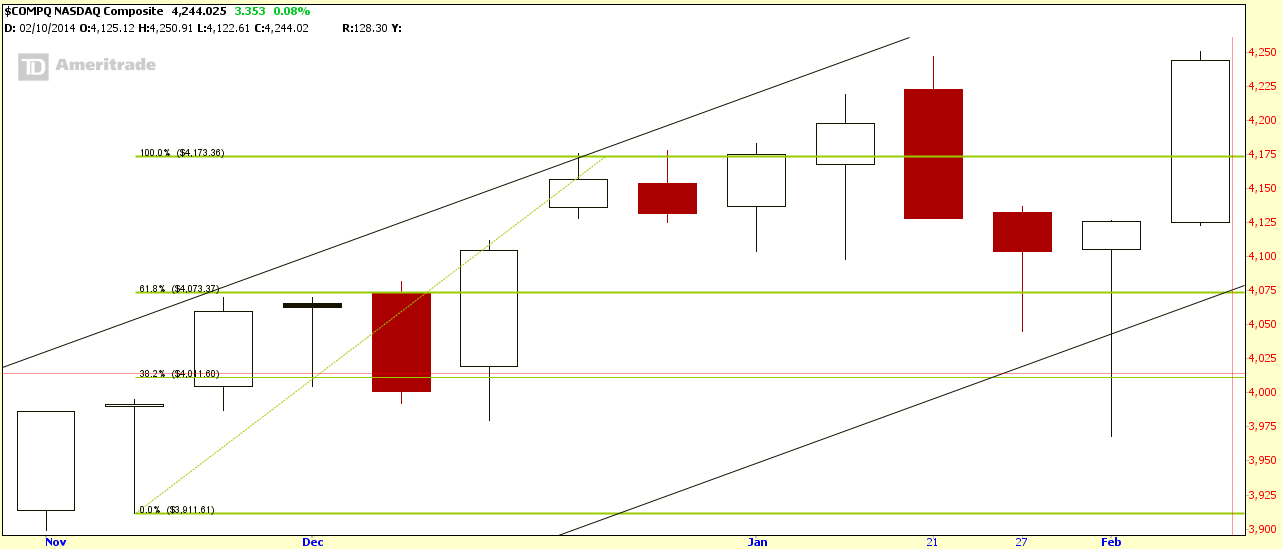

- Nasdaq Composite +1.6% YTD

- S&P 500 -0.5% YTD

- Russell 2000 -1.1% YTD

- Dow Jones Industrial Average -2.6%

Market Internals

Leaders & Laggards

Technical Updates

Weekly Updates

Next week in view

Alvin's commentary:

The market headed higher on Valentine's day! The Valentine's Day indicator has a 100% reliability over the last 25 years! Market started with a slight bearish tone and crawl its way back to end positive, perhaps an indication of the whole 2014 if the Valentine's Day indicator were to continue to be 100% accurate. Most notable is Nasdaq which struggle to stay positive and only manage to break positive at around 2pm.

Market Call: UP

Date: 18 Feb 2014

No comments:

Post a Comment