Market Summary

After enduring a broad-based selloff on Monday, the stock market rebounded, erasing roughly a third of yesterday's losses. The Nasdaq led the way, rising 0.9% while the S&P 500 gained 0.8%. For its part, the Dow Jones Industrial Average added 0.5%, but was unable to reclaim its 200-day moving average (15474).

Equities rallied steadily throughout the session in the absence of yen strength, which has been a headwind to the market since the start of the year. In fact, the yen began retreating overnight, and continued its slide into the close. Dollar/yen finished near 101.65 after starting its rally from just below the 101.00 level. Meanwhile yen futures lost 0.8%, trimming their 2014 gain to 3.6%.

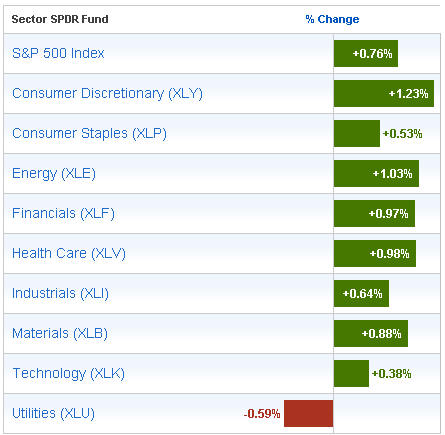

Nine of ten sectors ended in the green with the discretionary space in the lead. The sector added 1.2% after Michael Kors (KORS 89.91, +13.24) and Yum! Brands (YUM 72.06, +5.06) reported above-consensus earnings. KORS surged 17.3% and YUM jumped 8.9% while also providing support to their respective industry groups. Despite today's relative strength, the discretionary sector remains the weakest performer of the year, down 7.4%.

Other influential groups like health care (+1.0%) and financials (+1.0%) also finished ahead of the broader market while technology (+0.5%) and industrials (+0.6%) lagged.

The largest S&P 500 sector, technology, struggled to keep pace with the market even with its top component, Apple (AAPL 508.79, +7.26), advancing 1.5%. Another large sector member, Microsoft (MSFT 36.35, -0.13), ended little changed after announcing Satya Nadella will replace the outgoing Chief Executive Officer Steve Ballmer.

Elsewhere, the industrial sector lagged as the underperformance of Boeing (BA 122.04, -1.04) and United Technologies (UTX 109.10, -1.06) overshadowed the broad gains among transports. The Dow Jones Transportation Average advanced 1.2% as all but one component ended in the green. Con-way (CNW 37.19, -0.66) was the lone decliner, falling 1.7%.

Treasuries ended near their lows with the 10-yr yield up four basis points at 2.62%.

Participation was above average as 820 million shares changed hands at the NYSE.

Today's economic data was limited to the December factory orders report:

Equities rallied steadily throughout the session in the absence of yen strength, which has been a headwind to the market since the start of the year. In fact, the yen began retreating overnight, and continued its slide into the close. Dollar/yen finished near 101.65 after starting its rally from just below the 101.00 level. Meanwhile yen futures lost 0.8%, trimming their 2014 gain to 3.6%.

Nine of ten sectors ended in the green with the discretionary space in the lead. The sector added 1.2% after Michael Kors (KORS 89.91, +13.24) and Yum! Brands (YUM 72.06, +5.06) reported above-consensus earnings. KORS surged 17.3% and YUM jumped 8.9% while also providing support to their respective industry groups. Despite today's relative strength, the discretionary sector remains the weakest performer of the year, down 7.4%.

Other influential groups like health care (+1.0%) and financials (+1.0%) also finished ahead of the broader market while technology (+0.5%) and industrials (+0.6%) lagged.

The largest S&P 500 sector, technology, struggled to keep pace with the market even with its top component, Apple (AAPL 508.79, +7.26), advancing 1.5%. Another large sector member, Microsoft (MSFT 36.35, -0.13), ended little changed after announcing Satya Nadella will replace the outgoing Chief Executive Officer Steve Ballmer.

Elsewhere, the industrial sector lagged as the underperformance of Boeing (BA 122.04, -1.04) and United Technologies (UTX 109.10, -1.06) overshadowed the broad gains among transports. The Dow Jones Transportation Average advanced 1.2% as all but one component ended in the green. Con-way (CNW 37.19, -0.66) was the lone decliner, falling 1.7%.

Treasuries ended near their lows with the 10-yr yield up four basis points at 2.62%.

Participation was above average as 820 million shares changed hands at the NYSE.

Today's economic data was limited to the December factory orders report:

- Factory orders declined 1.5% after increasing a downwardly revised 1.5% (from 1.8%) in November. The Briefing.com consensus expected factory orders to decline 1.7%. The durable goods data were revised slightly higher, but still left a lot to be desired. Orders fell 4.2%, which was slightly above the 4.3% decline reported in the advance release. A large portion of the decline was a result of a sharp drop in transportation demand (-9.7%), which was mostly the result of a 16.9% decline in defense and nondefense aircraft.

- Nasdaq Composite -3.5% YTD

- S&P 500 -5.0% YTD

- Russell 2000 -5.1% YTD

- Dow Jones Industrial Average -6.8% YTD

Market Internals

Leaders & Laggards

Technical Summary

Next Day in view

Alvin's commentaries

As expected, some short covering after DFDM. Market started with a bullish bias which quickly faded after 1pm. Today we are expecting the ADP, which I am not holding my breath, do expect some volatility.

Market Call: UP

Date: 4 Feb 2014

No comments:

Post a Comment